At some point, nearly every business will face cash flow challenges for a variety of reasons. A slow-paying customer, unexpected expenses, import tariffs, seasonal dips in revenue, or even rapid growth can all create temporary strain on working capital.

During these periods, business owners often prioritize immediate operating expenses, viewing payroll, rent, and vendors as more urgent while federal or state tax payments feel like something that can wait. But when tax obligations begin to fall behind, understanding how to manage the situation with the IRS before a federal tax lien is filed becomes critical — especially if you want to preserve access to business financing and the working capital you need to operate.

If mounting tax arrears are causing concern, early action is essential. Tax balances accumulate penalties and interest, and once the IRS files a tax lien, it will significantly restrict your company’s ability to secure financing. What may begin as a temporary cash flow issue can quickly escalate into a formal IRS tax lien that limits funding options and places additional pressure on the business.

What Happens When the IRS Files a Tax Lien?

When the IRS files a Notice of Federal Tax Lien, it becomes a public record. More importantly, it establishes the IRS as a priority creditor.

In practical terms, this means:

Secured Interest Without Consent

The IRS gains a secured interest in your business assets without requiring your consent or approval

Lien Attaches to ALL Business Assets

The lien attaches to all your assets, including accounts receivable and other property

IRS Takes Priority

Once a federal tax lien is filed, the IRS moves ahead of other lenders in repayment priority

Prior UCC Filings Lose Priority

Even lenders with prior UCCs filing will be superseded

This priority status dramatically changes the risk profile of your business from a lender’s perspective.

Once a tax lien is filed, securing working capital becomes significantly more difficult. Financing options narrow substantially until the lien is resolved or addressed through a formal agreement with the IRS. At that stage, the limited lenders willing to provide funding typically charge premium rates and impose restrictive terms due to the elevated risk, increasing the overall cost of capital for the business.

In more severe situations, continued inaction can push a business toward insolvency. While Chapter 11 bankruptcy protection is sometimes necessary, it is typically expensive, time-consuming, and difficult to structure quickly in a way that preserves operational stability. Legal fees, court oversight, and restructuring requirements can create additional pressure at a time when speed and flexibility are critical. For most businesses, avoiding that path altogether by addressing tax issues early is far preferable.

The Critical Difference: Before vs. After a Tax Lien Is Filed

There is a major difference between:

Falling behind on taxes

and

Having a federal tax lien filed

Before a lien is recorded, lenders have more flexibility to structure funding solutions. After filing, legal priority issues complicate approvals and increase underwriting risk.

Acting early can preserve:

- Access to invoice factoring

- Accounts receivable financing

- Asset-based lending

- Bank line of credit

- Other forms of working capital

Waiting until a lien appears on public record often means fewer options, more documentation requirements, and longer approval timelines.

Why Tax Liens Affect Business Funding:

Lenders evaluate risk based on priority of repayment. When the IRS holds first position on business assets, it limits the collateral available to secure financing.

Even if your company is profitable and growing, a filed tax lien introduces:

- Increased legal complexity

- Potential asset encumbrance

- Subordination requirements

- Higher perceived default risk

For many financing providers, that can be a deal breaker.

This is why proactive planning matters.

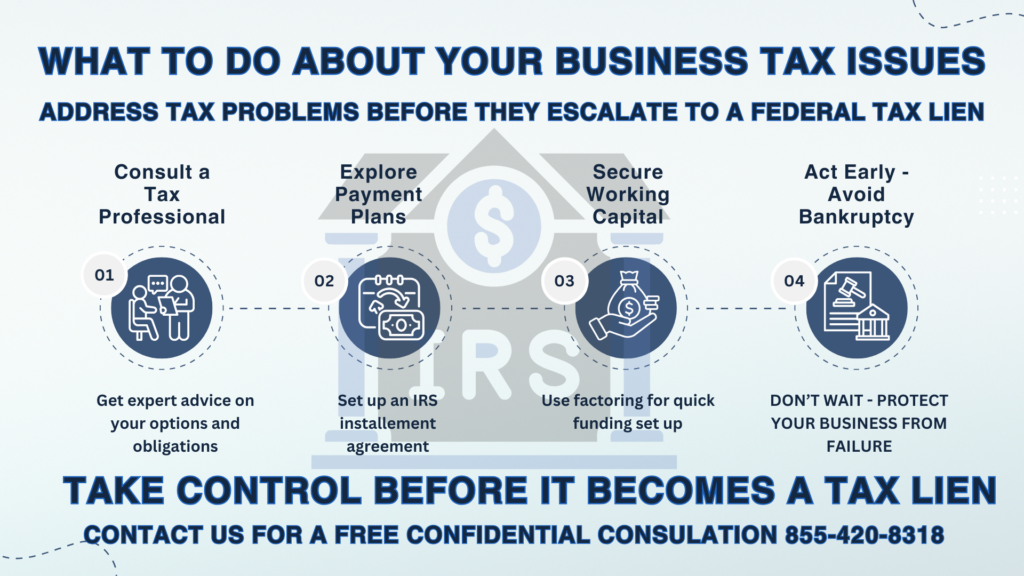

What Business Owners Should Do If They’re Behind on Taxes

If you’re experiencing temporary tax challenges, consider these steps immediately:

- Speak with a qualified tax professional who regularly handles IRS tax arrears and lien situations. Early professional guidance can help you negotiate payment arrangements and prevent the issue from escalating into a formal lien that restricts access to funding.

- Explore IRS payment plan options to avoid allowing the situation to progress to lien filing

- Evaluate financing solutions before a lien is recorded

Many businesses turn to working capital funding solutions to stabilize cash flow before formal enforcement actions occur. Invoice factoring, or accounts receivable funding, can be the perfect solution, offering a fast and flexible option, allowing companies to convert outstanding receivables into immediate cash much quicker than obtaining traditional bank financing. Because approval is primarily based on the creditworthiness of your customers rather than your balance sheet strength or profitability, factoring can frequently be implemented in days, not weeks or months, and without the excessive fees or burdensome long-term costs sometimes associated with higher-risk lending products. The key is timing.

Can You Get Financing With a Tax Lien?

In some situations, yes — but it is considerably more complex and will likely be more expensive.

It may require:

- Formal IRS payment agreements

- Subordination requests

- Direct pay arrangements

- Additional legal documentation

Each of these adds time, cost, and uncertainty.

It is far simpler to secure funding before the IRS establishes priority and agree a manageable payment plan.

How Eagle Business Credit Helps Businesses Navigate Cash Flow Challenges

At Eagle Business Credit, we work with companies across a wide range of industries that are navigating temporary cash flow pressure.

We understand that tax situations often stem from timing issues — not failing businesses. Our team evaluates each opportunity individually and, where appropriate, can structure working capital solutions designed to:

➤ Improve cash flow predictability

➤ Accelerate payment on your receivables

➤ Stabilize operations

➤ Support long-term recovery and business growth

The earlier the initial conversation happens, the more options typically remain available.

How to Stay Out of Financial Trouble

At Eagle Business Credit, we help businesses stay ahead of cash flow challenges by providing fast, flexible working capital through invoice factoring. Instead of waiting 30, 60, or even 90 days to get paid by customers, you get cash immediately to cover payroll, rent, supplies, and more.

The Bottom Line: Act Before a Tax Lien Limits Your Options

Once a federal tax lien is recorded, the IRS steps into priority position ahead of other secured creditors. That shift can dramatically reduce your financing flexibility, increase your cost of capital, and narrow your available funding options.

Before a lien is filed, solutions are typically faster, simpler, and more affordable. After filing, financing often becomes legally complex, more restrictive, and significantly more expensive.

Tax issues do not resolve themselves and waiting rarely improves the outcome.

If you are concerned about falling behind on taxes, unsure how to catch up on mounting arrears, or simply want to protect your company’s access to working capital, the most important step is starting the conversation early.

At Eagle Business Credit, we evaluate each situation individually and focus on practical, real-world solutions that stabilize cash flow and preserve financing flexibility.

A confidential discussion today could make the difference between maintaining control — or reacting to limited options later.

Contact our team to explore your options before the situation escalates.

Need help with your cash flow?

Talk to the team at Eagle Business Credit today to see how invoice financing can work for you and is always one of the best funding option for small businesses whatever the economy is doing.

Call us at (855) 420-8318

www.eaglebusinesscredit.com

Useful Links to Other Articles:

The Relationship Between Working Capital Management & Business Success

The Importance of Working Capital in Business OperationsWhat the Spike in Chapter 11 Bankruptcies Means for Your Business

What the Spike in Chapter 11 Bankruptcies Means for Your Business