For small business owners seeking funding options, new entrepreneurs embarking on their journey, and even those grappling with poor business credit, understanding the significance of a business credit score is a fundamental step towards securing financial stability and growth. Much like a personal credit score influences individual borrowing, a business credit score is a metric that holds sway over a company’s ability to access financing and favorable terms. In this article, we’ll unravel the complexities of a business credit score, its impact, and strategies to enhance it.

What Is a Business Credit Score?

In the world of commerce, a business credit score is like a report card that evaluates the financial health and reliability of a business entity. It provides potential lenders, suppliers, and partners with insights into how responsibly a business manages its financial obligations. Unlike a personal credit score, which assesses an individual’s financial history, a business credit score focuses exclusively on a company’s creditworthiness.

Similarities to a Personal Credit Score

Just as an individual’s credit score influences loan approvals and interest rates, a business credit score plays a pivotal role in determining the amount and terms of financing available to a business. It’s a reflection of how diligently a business meets its financial commitments, which could encompass loans, credit lines, leases, and supplier payments. A higher business credit score indicates a lower risk for lenders, resulting in more favorable borrowing conditions.

What Shapes a Business Credit Score?

Several factors contribute to the determination of a business credit score, and while the exact calculation methods may vary among credit reporting agencies, the general principles remain consistent:

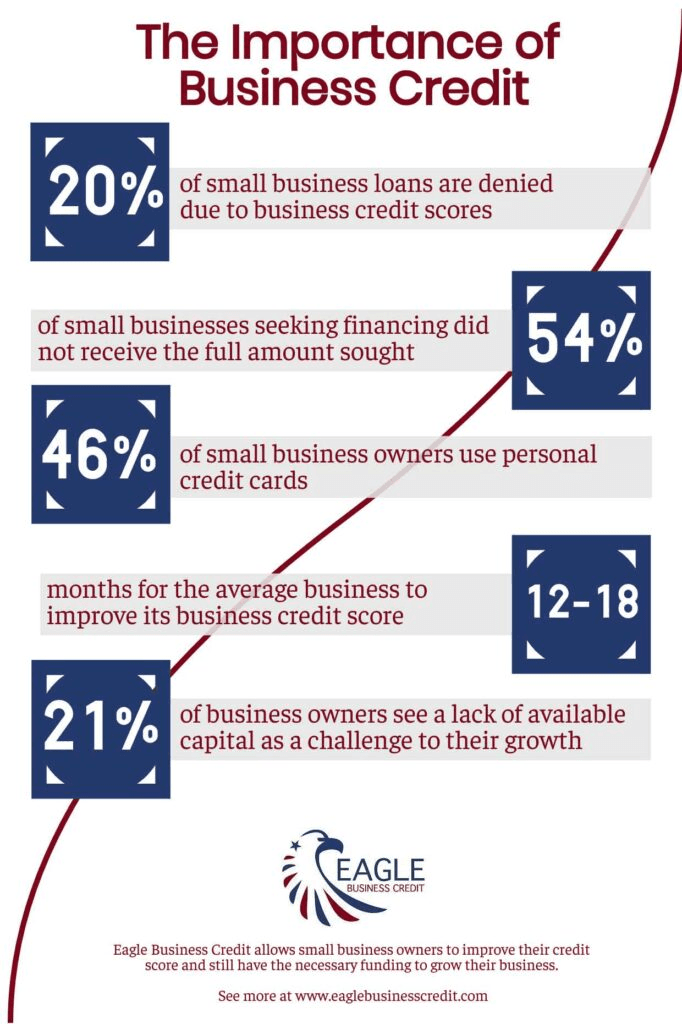

- Payment History: Timely payments on outstanding debts are a cornerstone of a healthy business credit score. Consistently meeting payment deadlines demonstrates financial responsibility and reliability.

- Age of Credit History: Just as a longer personal credit history is seen as more stable, a longer business credit history can positively impact your score.

- Debt Levels: The ratio of outstanding debt to available credit, known as the credit utilization ratio, is an essential metric. High levels of debt in relation to credit limits can be viewed negatively.

- Public Records: Any legal actions, liens, judgments, or bankruptcies against your business can significantly affect your credit score.

- Industry Risk and Company Size: The nature of your industry and the size of your business also influence your credit score. Industries with higher perceived risk factors may face greater scrutiny.

Improving Your Business Credit Score

For entrepreneurs looking to bolster their business credit score, a proactive approach is essential. Here are some strategies to consider:

- Timely Payments: Consistently make payments on time or, even better, ahead of schedule. This demonstrates reliability and builds a strong credit history.

- Credit Utilization: Avoid maxing out credit lines and aim to keep credit utilization below 30% to show responsible financial management.

- Monitor Your Credit Report: Regularly review your business credit report for inaccuracies or discrepancies that might be impacting your score negatively.

- Diversify Credit Types: A mix of credit types, such as trade credit, loans, and credit cards, can positively influence your score.

- Build Relationships: Maintain healthy relationships with suppliers, partners, and creditors, as they can provide positive references that contribute to your credit profile.

- Improve Cash Flow: Having healthy cash flow is the key to being able to meet repayments early.

Small business owners looking to improve their business credit can use invoice factoring to help. Factoring your receivables in addition to maintaining a strong payment history, managing credit utilization ratios, and diversifying credit types can put you on the road to better business credit.

Here’s how invoice factoring can contribute to improving your business credit over time:

- Establishing a Positive Payment History: When you engage in invoice factoring, the factoring company assesses the creditworthiness of your clients before purchasing your invoices. This means that you’re essentially partnering with a company that evaluates the payment history of your customers. By working with clients who consistently pay on time, you indirectly contribute to building a positive payment history for your business.

- Improving Cash Flow Management: Invoice factoring provides your business with immediate cash for your outstanding invoices. This improved cash flow can help you meet your financial obligations, including paying suppliers, lenders, and other creditors on time. Demonstrating a consistent ability to meet these obligations can contribute to a positive credit profile.

- Reducing Financial Stress: Improved cash flow resulting from invoice factoring can lead to reduced financial stress and better overall financial management. This can have indirect benefits for your creditworthiness, as financial stability is a key factor in credit assessments.

- Opportunity for Growth: Access to quick capital through invoice factoring can allow your business to take advantage of growth opportunities, invest in expansion, and cover operational expenses. Successfully utilizing these funds can lead to increased revenue and profitability, which can have a positive impact on your credit profile.

- Potential for Referrals: Establishing a positive relationship with a reputable factoring company can lead to potential referrals and recommendations. These references can contribute to a positive credit reputation when lenders or credit agencies assess your business.

In conclusion, a business credit score is a crucial element that shapes a company’s financial landscape. It affects the availability and terms of funding, making it a vital consideration for both established businesses and startups. By adhering to responsible financial practices, focusing on payment history, prudent credit utilization, and consistently monitoring and improving credit profiles, entrepreneurs can pave the way for a brighter financial future. Whether you’re seeking funding, just starting out, or working to overcome credit challenges, understanding and proactively managing your business credit score is a powerful tool for success. Invoice factoring can help contribute to positive credit management and higher business credit.